New Year, New Limits: 2026 Limits for Retirement Plans and Annual Review

This article was written by Planning Supervisor Diane Krainik, CFP®.

As a new year begins, it is a good time to review your employer plans and make sure you are on track for your savings goals. It is also important to recognize any changes to the tax code that may now be a factor.

For 2026, you’ll be able to add more to your 401(k), 403(b), 457 plans, and the federal government’s Thrift Savings Plan. The contribution limit increases to $24,500, up from $23,500. There is an $8,000 catch-up if you’re 50 or older. People who are 60 to 63 can contribute an additional $11,250 in 2026 in lieu of the $8,000, if your plan allows.

One caveat: In 2026, a provision in the Secure 2.0 retirement legislation mandates workers who are 50 and older and earned more than $150,000 in the previous year make catch-up contributions on an after-tax basis in a Roth account in their employer-sponsored retirement plans if the option is offered.

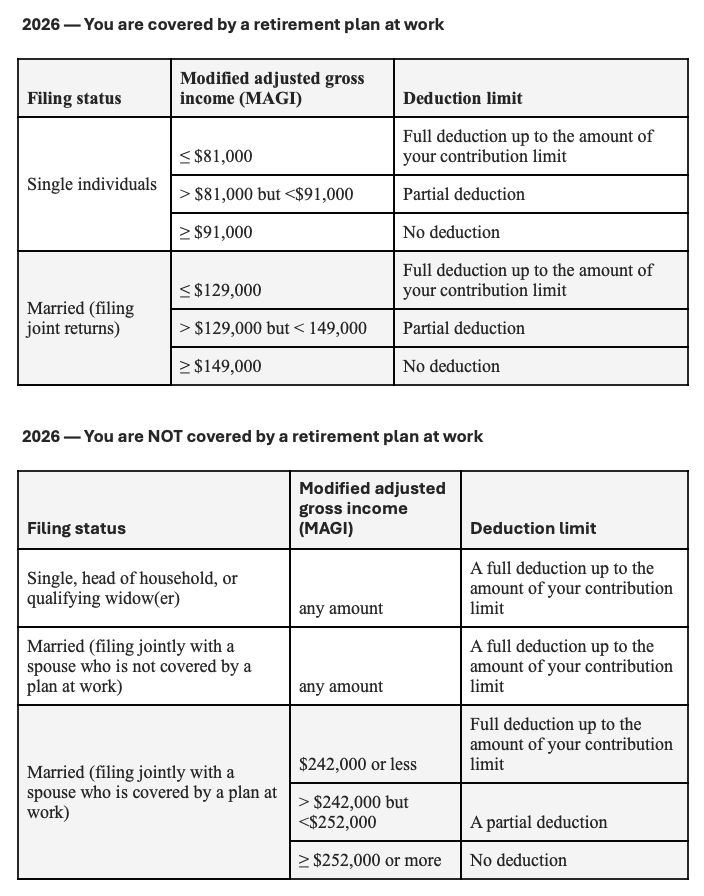

If your employer’s plan doesn’t offer a Roth 401(k) account, you may still be able to contribute your catch-up amount to a Roth IRA if your income is below the IRS income threshold. For 2026, single filers must have a modified adjusted gross income (MAGI) of less than $153,000, and joint filers less than $242,000, to make a full contribution.

Another thing for high earners to keep in mind is the inclusion of a true-up provision in your plan. A 401(k) retirement plan with a “true-up” is a provision where the employer reconciles matching contributions at the end of the year to ensure employees receive their full entitled match, even if they front-load contributions or contribute unevenly. It compensates for shortfalls that occur when employers match on a per-pay-period basis but base total eligibility on annual salary. If your plan does not have this provision, you will want to verify your contribution schedule to achieve maximum matching of employer funds prior to reaching the compensation cap of $360,000. This situation often occurs if you receive an annual bonus in the first part of the year.

Now that your limits are calculated, your investment strategy can be optimized. Your 401k website will have a list of investment options, and these may have changed during the year. It is important to communicate this information to your advisor, so your plan is coordinated across all assets. Having appropriate asset classes working in specific asset categories is important for tax efficiency and overall strategic alignment. Market fluctuations can cause your portfolio to drift from its intended asset allocation.

Non-employer retirement plan limits have also been increased. For 2026, the spousal IRA contribution limit is $7,500 for those under 50, with an additional $1,100 catch-up for age 50+, totaling $8,600, allowing a working spouse to fund an IRA for a non-working spouse if they have sufficient earned income (at least the total contribution amount). This means a couple could save up to $15,000 ($7,500 each) or $17,200 ($8,600 each) if both are 50+, provided the working spouse earns enough to cover both.

Designation of beneficiary and contingent beneficiary is also an important thing to review. Not having these listed could lead to a big headache if something were to happen to you. Having this buttoned up provides several benefits:

- Avoids Probate - Assets with a designated beneficiary bypass probate, the legal process of administering a deceased person’s estate. This allows your loved ones to access the funds much faster, avoiding a process that can be time-consuming, costly, and public.

- Ensures Your Wishes Are Honored - Beneficiary designations generally take precedence over instructions in a will. If you don’t name a beneficiary, state law or the plan’s default rules will determine who receives your assets, which may not align with your actual intentions (e.g., assets could go to an ex-spouse or an unintended relative).

- Provides Legal Control - By naming a beneficiary, you retain control over your assets after your death, choosing who gets them and in what proportions. You can name individuals, a trust, or even a charitable organization.

- Potential Tax Efficiency - Naming a beneficiary, particularly a spouse, can offer favorable tax options, such as the ability to roll over the inherited funds into their own retirement account and potentially delay required minimum distributions (RMDs).

- Protects Assets from Creditors - Assets that pass directly to a named beneficiary typically avoid the claims of your estate’s creditors.

- Minimizing Family Conflict - Clear and up-to-date beneficiary designations help prevent confusion and potential legal battles among family members during an already difficult time.

- Designate Both Primary and Contingent Beneficiaries - A primary beneficiary is first in line to receive the assets. A contingent (secondary) beneficiary is a backup who inherits the funds if the primary beneficiary is deceased or cannot be located.

Annual maintenance is important for your home, your health and your investments. Be sure to check in with us if any changes have occurred or are anticipated.